All Categories

Featured

Table of Contents

The are entire life insurance policy and universal life insurance coverage. expands cash money worth at an assured rate of interest and also via non-guaranteed returns. grows money worth at a fixed or variable rate, depending on the insurance company and policy terms. The cash money worth is not contributed to the fatality advantage. Money value is a feature you make use of while to life.

After 10 years, the money value has expanded to about $150,000. He obtains a tax-free car loan of $50,000 to begin a company with his bro. The plan funding interest rate is 6%. He repays the loan over the following 5 years. Going this route, the rate of interest he pays returns into his policy's money worth rather than a financial organization.

How Does Infinite Banking Work

The principle of Infinite Banking was developed by Nelson Nash in the 1980s. Nash was a finance specialist and follower of the Austrian school of economics, which advocates that the value of products aren't clearly the result of standard financial structures like supply and need. Instead, people value money and products in different ways based upon their economic standing and needs.

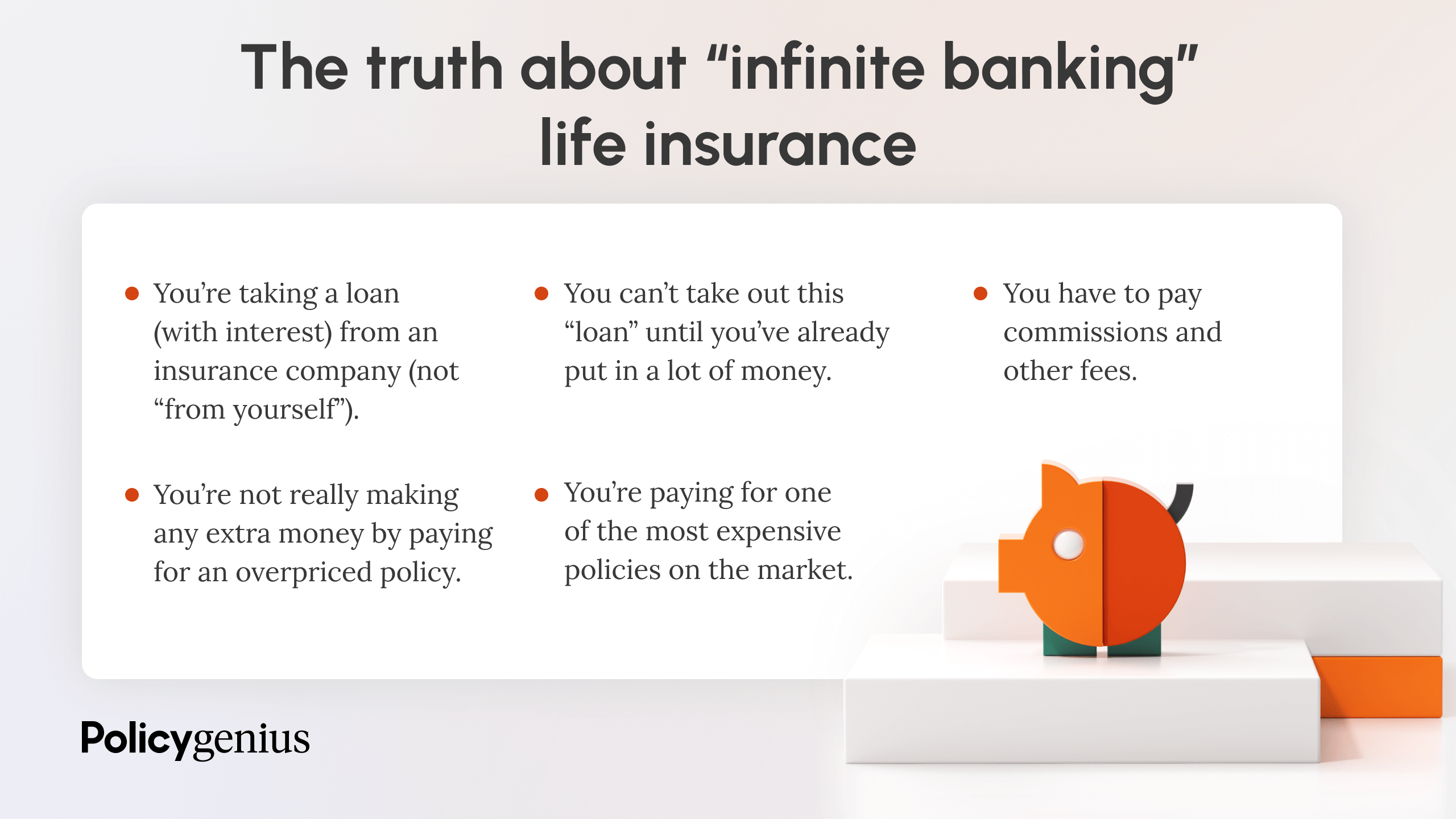

One of the mistakes of conventional banking, according to Nash, was high-interest rates on fundings. Long as banks set the rate of interest prices and car loan terms, individuals didn't have control over their very own riches.

Infinite Financial requires you to have your financial future. For ambitious individuals, it can be the most effective monetary tool ever. Here are the advantages of Infinite Financial: Arguably the single most beneficial element of Infinite Banking is that it enhances your capital. You do not require to experience the hoops of a typical bank to obtain a car loan; simply demand a plan funding from your life insurance policy firm and funds will certainly be offered to you.

Dividend-paying whole life insurance policy is really low threat and offers you, the insurance holder, a good deal of control. The control that Infinite Banking uses can best be grouped into two categories: tax advantages and possession defenses - infinite bank statement. Among the factors whole life insurance policy is excellent for Infinite Banking is how it's exhausted.

Infinite Banking Canada

When you utilize entire life insurance for Infinite Financial, you participate in a private agreement between you and your insurance provider. This privacy offers particular property protections not discovered in other economic lorries. Although these securities may differ from one state to another, they can consist of protection from asset searches and seizures, protection from reasonings and security from lenders.

Entire life insurance coverage policies are non-correlated properties. This is why they work so well as the financial structure of Infinite Financial. Regardless of what happens in the market (supply, genuine estate, or otherwise), your insurance policy keeps its worth.

Market-based financial investments expand wide range much faster yet are subjected to market variations, making them naturally risky. What if there were a third bucket that provided security yet likewise modest, surefire returns? Whole life insurance coverage is that third pail. Not just is the price of return on your entire life insurance policy ensured, your fatality advantage and costs are also guaranteed.

This framework aligns completely with the concepts of the Continuous Wealth Approach. Infinite Banking interest those looking for higher economic control. Right here are its main benefits: Liquidity and ease of access: Plan financings give instant access to funds without the limitations of typical financial institution fundings. Tax obligation efficiency: The money value expands tax-deferred, and policy fundings are tax-free, making it a tax-efficient tool for building wealth.

Infinite Banking Wiki

Property protection: In lots of states, the cash worth of life insurance policy is secured from lenders, adding an extra layer of financial safety and security. While Infinite Banking has its qualities, it isn't a one-size-fits-all remedy, and it includes substantial disadvantages. Right here's why it might not be the most effective method: Infinite Banking usually calls for complex plan structuring, which can confuse policyholders.

Picture never having to stress concerning bank finances or high interest rates again. That's the power of unlimited financial life insurance coverage.

There's no set finance term, and you have the freedom to select the settlement timetable, which can be as leisurely as paying off the finance at the time of fatality. This versatility reaches the maintenance of the loans, where you can select interest-only payments, keeping the finance balance level and workable.

Holding money in an IUL dealt with account being credited rate of interest can often be far better than holding the money on down payment at a bank.: You've always imagined opening your very own bakeshop. You can borrow from your IUL policy to cover the first expenditures of leasing a space, acquiring equipment, and employing personnel.

Whole Life Infinite Banking

Personal fundings can be acquired from traditional financial institutions and debt unions. Borrowing cash on a credit scores card is usually extremely costly with annual percent rates of interest (APR) frequently reaching 20% to 30% or more a year.

The tax treatment of policy lendings can vary dramatically depending upon your country of residence and the specific regards to your IUL plan. In some regions, such as North America, the United Arab Emirates, and Saudi Arabia, policy finances are typically tax-free, providing a substantial benefit. In other jurisdictions, there might be tax obligation effects to take into consideration, such as prospective tax obligations on the loan.

Term life insurance coverage just provides a fatality benefit, without any type of cash worth accumulation. This indicates there's no cash money value to obtain against.

Nonetheless, for funding officers, the substantial guidelines enforced by the CFPB can be seen as cumbersome and restrictive. Initially, finance police officers frequently suggest that the CFPB's laws create unnecessary red tape, leading to even more documents and slower lending processing. Regulations like the TILA-RESPA Integrated Disclosure (TRID) regulation and the Ability-to-Repay (ATR) needs, while focused on shielding consumers, can bring about hold-ups in closing bargains and increased operational expenses.

{kind=link}

Latest Posts

Infinite Family Banking

Infinite Banking Wikipedia

'Be Your Own Bank' Mantra More Relevant Than Ever